Key Takeaways

- Expect to pay 6–10% of your home’s sale price in closing costs.

- Negotiate commissions and compare title and escrow services to save money.

- Cash offers can significantly reduce both costs and delays.

- Consult a tax professional early to plan for capital gains obligations.

- Prepare for surprises with a contingency fund to ensure a smooth close.

Understanding Closing Costs

Selling your home is often driven by the need for a swift and smooth transaction, yet understanding the financial aspects—especially closing costs—is crucial. Closing costs comprise various fees that can significantly impact your net proceeds when finalizing a real estate sale. These expenses commonly include agent commissions, title insurance, transfer taxes, escrow fees, and legal fees. For home sellers, it’s vital to know what to expect so you can plan effectively for a successful financial outcome. For those looking to expedite the selling process without unnecessary hurdles, resources like https://alaskanhomebuyers.com/sell-my-house-fast-chugiak-ak/ are helpful starting points to explore fast home-selling solutions in Chugiak and beyond.

On average, sellers might be responsible for 6% to 10% of their home’s sale price in closing costs. By proactively researching these figures and exploring your options, you are in a much stronger position to handle the process efficiently and confidently. Preparing ahead enables you to make informed decisions and avoid last-minute financial surprises.

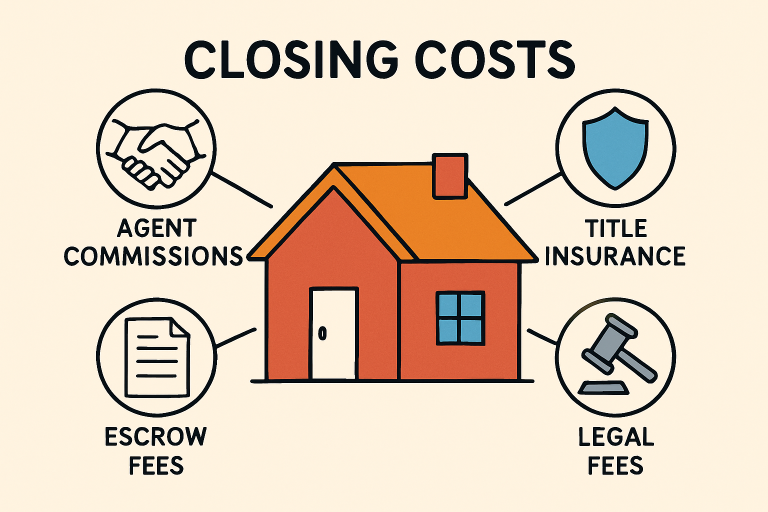

Breakdown of Common Seller Closing Costs

- Agent Commissions: Typically 5% to 6% of the sale price, divided between the buyer’s and seller’s real estate agents.

- Title Insurance: Protects against future legal claims over property ownership; fees vary depending on your state.

- Transfer Taxes: Required by state or local governments during property transfers, these can add up quickly in certain areas.

- Escrow Fees: Charged by the escrow company or attorney managing the sale transaction.

- Attorney Fees: Apply in states where having a lawyer involved in the closing is mandatory or preferred for additional protection.

Strategies to Reduce Closing Costs

Taking practical steps to reduce closing costs can noticeably impact your final profit. Here are proven approaches to trim these expenses:

1. Negotiate Agent Commissions

The largest seller closing cost is often the agent’s commission. Talk to your listing agent about lowering the commission rate. In today’s competitive markets, many agents are open to negotiation, especially if your property is move-in ready or located in a desirable neighborhood.

2. Shop Around for Service Providers

Title insurance and escrow costs vary widely between service providers, sometimes even within the same city. Obtain multiple quotes for these services before committing. Most states allow sellers to select their providers, empowering you to seek the best value.

3. Time Your Sale Strategically

The timing of your sale can influence your negotiation power. Listing your home during a buyer’s market, when buyers are eager and inventory is high, may allow sellers extra leverage in negotiating certain closing costs. Alternatively, selling in a seller’s market could prompt buyers to cover more costs, especially if bidding wars are common.

Leveraging Cash Offers to Expedite Sales

Cash offers play a significant role in reducing both closing time and associated costs. When buyers pay cash, many traditional mortgage-related fees—such as loan origination and lender-required repairs—are eliminated. Cash buyers frequently purchase homes “as-is,” sparing sellers the expense and hassle of last-minute repairs or upgrades. This makes accepting a cash offer appealing for homeowners looking for a streamlined sale without excessive fees or delays.

Companies like alaskanhomebuyers.comspecialize in helping sellers achieve quick, hassle-free transactions, providing fair cash offers for homes in any condition.

Understanding Tax Implications

Capital gains taxes can be a factor when you sell your home, especially if you have experienced significant appreciation in property value. However, if the home has served as your primary residence for at least two of the last five years, you may qualify for a capital gains exclusion—up to $250,000 for single filers or $500,000 for married couples. Consulting with a tax professional will help you clarify your eligibility and ensure you prepare for any liabilities before closing the sale.

Preparing for Unexpected Expenses

No matter how carefully you plan, unexpected costs can surface during closing. These might include minor repairs requested after inspection, last-minute title issues, or miscellaneous fees. Set aside a contingency fund to cover surprises, enabling you to avoid delays or renegotiations that can threaten a fast closing. Careful budgeting provides peace of mind and shields you from added stress during a pivotal financial transaction.

Final Thoughts

Effectively managing closing costs allows you to maximize your net proceeds and minimize the potential for frustration in fast-paced home sales. By thoroughly understanding the makeup of closing costs, actively seeking ways to reduce fees, embracing flexible options like cash offers, and anticipating potential tax implications, sellers can move forward with confidence. Prioritizing preparation and knowledgeable decision-making ensures a smoother, more profitable selling experience.

- How Scented Candles Elevate Home Ambiance and Promote Relaxation

- The Digital Revolution in Dental Laboratories: Transforming the Future of Dentistry

- The Ultimate Auto Accident Recovery Network: Top Businesses Working Together for Your Complete Care

- A Comprehensive Approach to Advanced Aesthetics and Personal Wellness

- How to Convert Your Bathtub Into a Shower: A Complete Guide